®

®

TaxReply India Private Limited

Best GST Library

Subscription Plans

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

HSN Codes

GST Forms

My Favourites New

GST Diary

GST Notebook

GST Staff Manager New

GST Fees Manager

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

16.06k

16.06k

Penalty for not carrying e-way bill during transportation of goods -

Section 122(1)(xiv) of CGST Act

Penalty for certain offenses

Where a taxable person who transports any taxable goods without the cover of documents as specified (e.g. e-way bill), he shall be liable to pay a penalty of Rs.10,000 or an amount equivalent to the tax evaded, whichever is higher.

Therefore minimum penalty for not carrying the e-way bill shall be Rs.10,000.

Reference - Section 122 of CGST Act

Section 129(1) of CGST Act

Detention, seizure and release of goods and conveyance in transit

Where any person transports any goods or stores any goods (in transit) in contravention of the provisions of this Act or the rules made thereunder, all such goods and conveyance shall be liable to detention or seizure. After detention or seizure, it shall be released on payment of below amount -

Where the owner of the goods comes forward for payment of tax and penalty:

-

In case of Taxable goods - Applicable tax on such goods + Penalty equal to 100% of the tax payable on such goods.

- In case of Exempted goods - 2% of value of goods or Rs.25,000, whichever is less

Where the owner of the goods does not come forward for payment of tax and penalty:

-

In case of Taxable goods - Applicable tax on such goods + Penalty equal to 50% of the value of goods reduced by the tax amount paid thereon

- In case of Exempted goods - 5% of the value of goods or Rs.25,000, whichever is less,

Reference - Section 129 of CGST Act​

Section 122(3)(b) of CGST Act

Penalty for certain offenses

Any person who acquires possession of, or in any way concerns himself in transporting, removing, depositing, keeping, concealing, supplying, or purchasing or in any other manner deals with any goods which he knows or has reasons to believe are liable to confiscation under this Act or the rules shall be liable to a penalty which may extend to twenty-five thousand rupees.

Reference - Section 122 of CGST Act

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

TaxReply

Jun 1, 2018

Comments

Dec 28, 2022

Jun 2, 2024

Post your comment here !

|

Login to Comment

|

Other Important Updates

GSTN Advisory on filing of SPL-01/ SPL-02 where payment details and demand amount are not matched.

12 Jun 2025

4.56k

12 Jun 2025

4.56k

GSTN Advisory on filing of Amnesty applications under Section 128A of the CGST Act

11 Jun 2025

3.28k

GSTN Advisory on System Validation for Filing of Refund Applications on GST Portal for QRMP Taxpayers

10 Jun 2025

3.07k

DIN not required for any document issued via GST Portal having verifiable RFN (Reference Number): CBIC New Circular

10 Jun 2025

4.95k

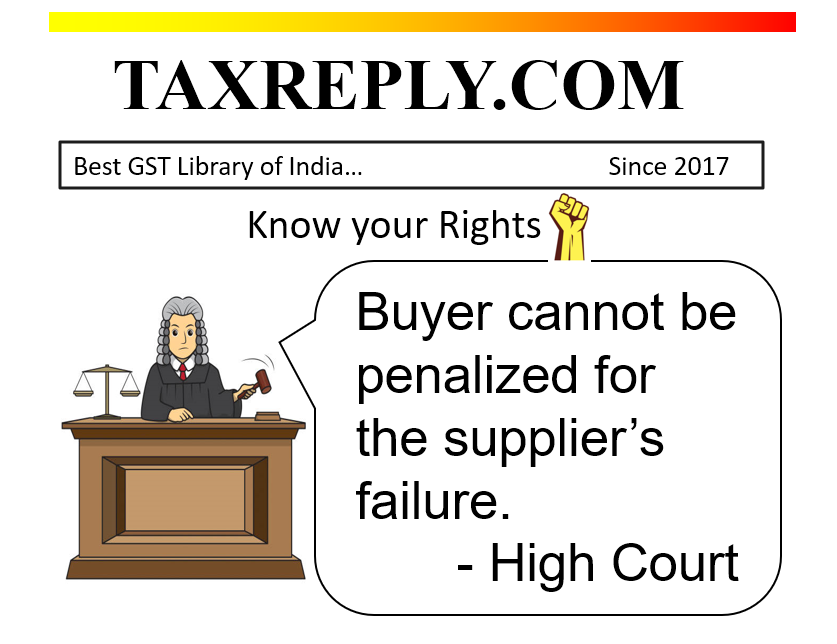

Buyer cannot be penalized for the supplier’s failure to deposit tax or file returns: High Court

9 Jun 2025

10.68k

GSTN Advisory - Hard Locking (Non-editable) Auto-populated liability in GSTR-3B from July 2025

7 Jun 2025

7.36k

High Court imposes penalty of Rs.1 lakh on GST Department for passing order without considering submission of taxpayer.

31 May 2025

30.03k

|

☛ Read more updates...

|

Jun

20 Jun

☑ Monthly | GSTR-3B

GSTR-3B for the m/o May 2025 (Monthly Taxpayer - Rule 61) - Either Compulsory taxpayer > 5 cr. or Voluntary taxpayer < 5 cr.

☑ Monthly | GSTR-5A

GSTR-5A for the m/o May 2025 [Return by OIDAR Service Providers - Rule 64.]

25 Jun

☑ Monthly | PMT-06

PMT-06 Monthly tax payment for May 2025 under QRMP Scheme [Rule 61(1)(ii) - Proviso to Section 39(7)].

Taxpayers have a choice to pay tax either, as per -

28 Jun

☑ Monthly | GSTR-11

GSTR-11 for the m/o May 2025 (Statement of inward supplies by persons having Unique Identification Number (UIN)).

30 Jun

☑ Annual | GSTR-4

GSTR-4 (Annual Return) for FY 2024-25 by Composite Taxpayer (Rule 62).