®

®

TaxReply India Private Limited

Best GST Library

Subscription Plans

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

HSN Codes

GST Forms

My Favourites New

GST Diary

GST Notebook

GST Staff Manager New

GST Fees Manager

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

8.56k

8.56k

Misconception vs. Reality (Rule 86B)

CBIC Clarifications on 1% cash payment under Rule 86B

Misconception 01:Large number of taxpayers would be affected.Reality:The rule provides for various exemptions like exporters, suppliers of goods of inverted duty structure, taxpayers having a footprint in the income tax database etc. It is expected that this rule would be applicable to less than 0.5% of total taxpayers base of 1.2 crore. The rule clearly identifies where the risk to revenue is high and imposes deterrence to the fraudsters in a multi-layered fraud of passing fake ITC. This rule would help to control such fraudsters, who issue fake invoices and show high turnovers but have no financial credibility and flee after misusing ITC without payment of any tax liability in cash. |

Misconception 02:The requirement of cash payment of 1% liability will create huge burden on small businesses and will increase their working capital requirement.Reality:The cash payment of 1% is to be calculated on the tax liability in a month and not turnover of the respective month. In fact, it amounts to only 0.01% of turnover. For example,, if a dealer has made sale of Rs. 1 crore of the goods whose tax rate is 12% and if he is discharging his tax liability more than 99% through ITC, then he has to pay only Rs 12,000 under this rule. On the other hand, a composition dealer would have paid Rs. 1 lakh in cash with this volume of sale. |

Misconception 03:This rule adversely affects small and medium enterprises.Reality:The new provision which restricts the use of ITC for discharging output liability is applicable to the registered person whose value of taxable supply other than exempt supply and export in a month exceeds Rs. 50 lakh - that means those annual whose turnover is more than Rs. 6 crore. Therefore, the rule does not apply to micro and small businessess and composition dealers. |

Misconception 04:All the registered persons will be required to pay 1% cash liability.Reality:The rule is applicable to only those registered persons whose value of taxable supply, other than exempt supply and export, in a month exceeds Rs. 50 lakh - that means those whose annual turnover is more than Rs. 6 Crore. This rule is also not applicable in the cases where the registered person:

|

Misconception 05:This rule adversely affects genuine taxpayers.Reality:This rule is only applicable to taxpayer who have taxable supplies or more than Rs. 50 lakh in a month, which amounts to an annual turnover of more than Rs. 6 crore. Besides, the registered persons failing in any of the exempted category including paying Rs. 1 lakh as income tax in each of the last two financial year or having received refund for more than Rs. 1 lakh in the previous year on account of export or inverted duty structure etc are also out of the purview of this rule. With this exemption and condition and precise targeting, the requirement of mandatory payment of at least 1% of the tax liability in cash would apply only to risky or suspicious taxpayer and genuine taxpayers would remain excluded. |

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

TaxReply

Dec 28, 2020

Comments

Dec 28, 2020

Dec 31, 2020

Post your comment here !

|

Login to Comment

|

Other Important Updates

3 years return restriction to be implemented from July 2025: File your pending return now: GSTN Advisory

18 Jun 2025

3.05k

18 Jun 2025

3.05k

GSTN Advisory on filing of SPL-01/ SPL-02 where payment details and demand amount are not matched.

12 Jun 2025

5.38k

GSTN Advisory on filing of Amnesty applications under Section 128A of the CGST Act

11 Jun 2025

3.46k

DIN not required for any document issued via GST Portal having verifiable RFN (Reference Number): CBIC New Circular

10 Jun 2025

5.21k

GSTN Advisory on System Validation for Filing of Refund Applications on GST Portal for QRMP Taxpayers

10 Jun 2025

3.11k

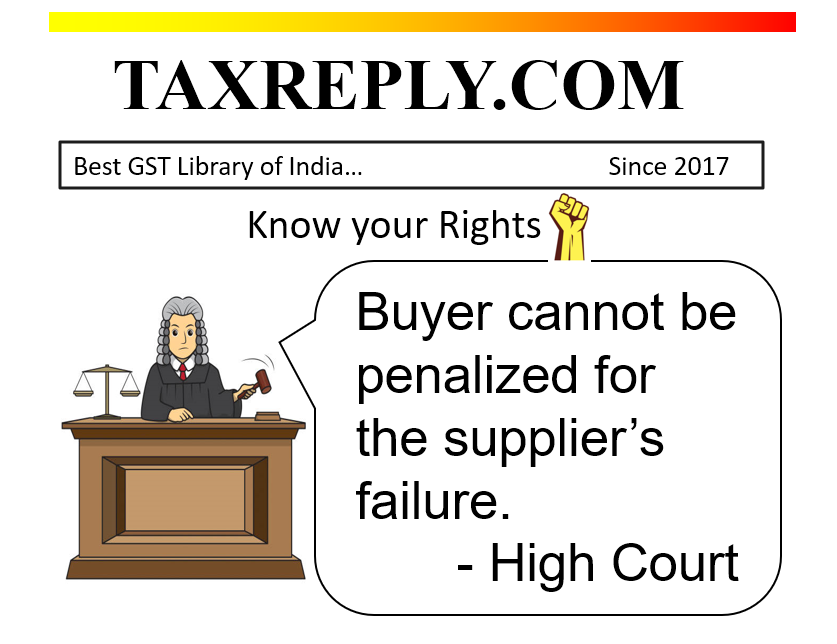

Buyer cannot be penalized for the supplier’s failure to deposit tax or file returns: High Court

9 Jun 2025

12.05k

|

☛ Read more updates...

|

Jun

25 Jun

☑ Monthly | PMT-06

PMT-06 Monthly tax payment for May 2025 under QRMP Scheme [Rule 61(1)(ii) - Proviso to Section 39(7)].

Taxpayers have a choice to pay tax either, as per -

28 Jun

☑ Monthly | GSTR-11

GSTR-11 for the m/o May 2025 (Statement of inward supplies by persons having Unique Identification Number (UIN)).

30 Jun

☑ Annual | GSTR-4

GSTR-4 (Annual Return) for FY 2024-25 by Composite Taxpayer (Rule 62).