®

®

TaxReply India Private Limited

Best GST Library

Subscription Plans

TaxGPT

GST News | Updates

GST Calendar

GST Case Laws

GST Case Laws Sitemap

GST Notifications, Circulars, Releases etc.

Act & Rules

Act & Rules (Multi-view)

GST Rates

HSN Codes

GST Forms

My Favourites New

GST Diary

GST Notebook

GST Staff Manager New

GST Fees Manager

GST Council Meetings

GST Set-off Calculator

ITC Reversal Calculator

E-invoice Calculator

Inverted Duty Calculator

GSTR-3B Manual

GSTR-9 Manual

GSTR-9C Manual

Full Site Search

E-way Bill

Finance Bill

GST e-books

®

®

Whatsapp

WhatsappGroup

@taxreply

TaxReplyCommunity

7.1k

7.1k

CBIC new Guidelines for launching of Prosecution under GST

Prosecution should not be launched indiscriminately against all the Directors of the company but should be restricted to only persons who oversaw day-to-day operations of the company and have taken active part in committing the tax evasion: Says CBIC

What is Prosecution?

Section 132 of the CGST Act codifies the offences under the Act which warrant institution of criminal proceedings and prosecution. Whoever commits any of the offences specified u/s 132(1) or 132(2) can be prosecuted.

Highlights of Guidelines?

2. Prosecution should not be launched in cases of technical nature, or where additional claim of tax is based on a difference of opinion regarding interpretation of law.

3. Further, the evidence collected should be adequate to establish beyond reasonable doubt that the person had guilty mind, knowledge of the offence, or had fraudulent intention or in any manner possessed mens-rea for committing the offence.

4. Prosecution should not be launched indiscriminately against all the Directors of the company but should be restricted to only persons who oversaw day-to-day operations of the company and have taken active part in committing the tax evasion etc. or had connived at it.

5. Prosecution complaint may even be filed before adjudication of the case, especially where offence involved is grave, or qualitative evidences are available, or it is apprehended that the concerned person may delay completion of adjudication proceedings.

6. In cases where any offender is arrested under section 69 of the CGST Act, 2017, prosecution complaint may be filed even before issuance of the Show Cause Notice.

7. Prosecution should normally be launched where amount of tax evasion, or misuse of ITC, or fraudulently obtained refund in relation to offences specified u/s 132(1) of the CGST Act, 2017 is more than Five Hundred Lakh rupees. However, in following cases, the said monetary limit shall not be applicable:

(i) Habitual evaders: Prosecution can be launched in the case of a company/taxpayer habitually involved in tax evasion or misusing Input Tax Credit (ITC) facility or fraudulently obtained refund. A company/taxpayer would be treated as habitual evader, if it has been involved in two or more cases of confirmed demand (at the first adjudication level or above) of tax evasion/fraudulent refund or misuse of ITC involving fraud, suppression of facts etc. in past two years such that the total tax evaded and/or total ITC misused and/or fraudulently obtained refund exceeds Five Hundred Lakh rupees. DIGIT database may be used to identify such habitual evaders.

(ii) Arrest Cases: Cases where during the course of investigation, arrests have been made under section 69 of the CGST Act.

|

☛ Login to read more...

|

:

:

Prosecution under GST

:

Criminal Offence

Digital GST Library

Plan starts from

₹ 5,000/-

(For 1 Year)

TaxReply

Sep 2, 2022

Post your comment here !

|

Login to Comment

|

Other Important Updates

GSTN Advisory on filing of SPL-01/ SPL-02 where payment details and demand amount are not matched.

12 Jun 2025

4.99k

12 Jun 2025

4.99k

GSTN Advisory on filing of Amnesty applications under Section 128A of the CGST Act

11 Jun 2025

3.31k

GSTN Advisory on System Validation for Filing of Refund Applications on GST Portal for QRMP Taxpayers

10 Jun 2025

3.08k

DIN not required for any document issued via GST Portal having verifiable RFN (Reference Number): CBIC New Circular

10 Jun 2025

5.07k

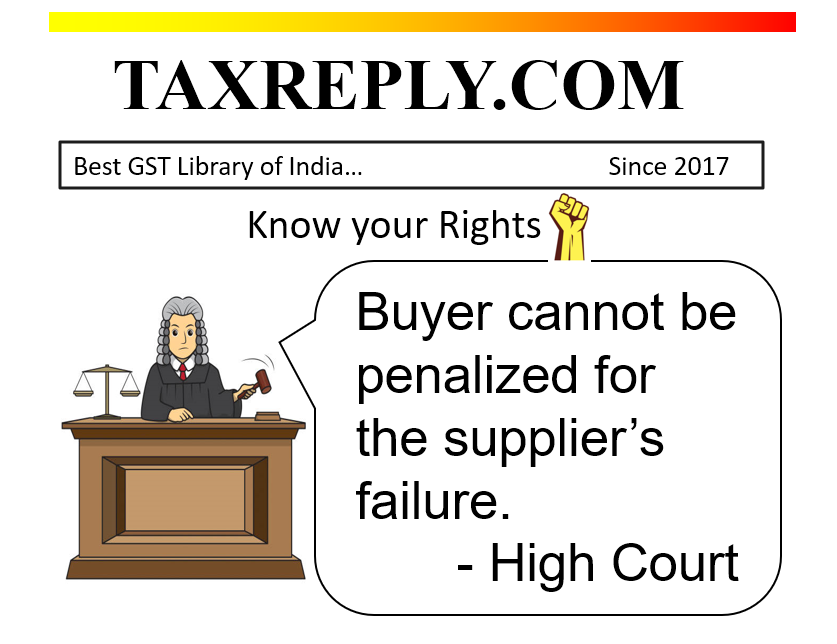

Buyer cannot be penalized for the supplier’s failure to deposit tax or file returns: High Court

9 Jun 2025

11.2k

GSTN Advisory - Hard Locking (Non-editable) Auto-populated liability in GSTR-3B from July 2025

7 Jun 2025

7.4k

High Court imposes penalty of Rs.1 lakh on GST Department for passing order without considering submission of taxpayer.

31 May 2025

30.1k

|

☛ Read more updates...

|

Jun

20 Jun

☑ Monthly | GSTR-3B

GSTR-3B for the m/o May 2025 (Monthly Taxpayer - Rule 61) - Either Compulsory taxpayer > 5 cr. or Voluntary taxpayer < 5 cr.

☑ Monthly | GSTR-5A

GSTR-5A for the m/o May 2025 [Return by OIDAR Service Providers - Rule 64.]

25 Jun

☑ Monthly | PMT-06

PMT-06 Monthly tax payment for May 2025 under QRMP Scheme [Rule 61(1)(ii) - Proviso to Section 39(7)].

Taxpayers have a choice to pay tax either, as per -

28 Jun

☑ Monthly | GSTR-11

GSTR-11 for the m/o May 2025 (Statement of inward supplies by persons having Unique Identification Number (UIN)).

30 Jun

☑ Annual | GSTR-4

GSTR-4 (Annual Return) for FY 2024-25 by Composite Taxpayer (Rule 62).